First Small Step Towards a Comprehensive Budget Reform

Summary: The sharp fall in Congress’ approval rating is a key indicator suggesting the need for congressional reform. The reform should respond to growing concerns that the institution is losing its ability to fulfill its legislative role granted by the Constitution. Given the fundamental roles of budget and oversight, keen attention should be paid to the improvement of budget procedures that reduce gridlock and avoid government shutdowns. Evaluating the causes leading to the current budget dysfunction and proposing solutions to increase the efficiency of a budget process should be the top priority of any reform effort. Because budget procedures impact all aspects of the legislative process, there is not a silver-bullet solution. Instead, reform must be comprised of different proposals for revision that will lead to lasting legislative and procedural change. Budget reform is complicated, since it has repercussions for nearly every aspect of governing. It is simple to say that Congress needs to reclaim its “power of the purse” but this is easier said than done. Having this in mind, our aim is to offer a list of measures and proposals, that while important on their own merits, will ultimately have to be considered in the context of a broader reform effort conducted by a Joint Committee on Congressional Reform that takes into account committee roles, the authorization process, appropriations and even the fiscal calendar. Changing the beginning of the fiscal year from October 1 to January 1 is an idea that has been discussed for many years and has broad support in Congress. It will be considered here as a component of the budget reform to help clarify the increasingly complex Federal budget process.

Introduction

To many, the words “congressional efficiency” are an oxymoron, akin to jumbo shrimp. Indeed, the authors of the Constitution deliberately set up an inefficient system of government, designed to govern by consensus, not raw majority power. But they did, nevertheless, assign certain essential functions of governing to the Legislature, the most important being the power to originate spending, taxes and borrowing – the responsibility to set the budget of the nation. Different studies show how Congress’ approval rates have dropped dramatically as respondents consider representatives’ work as obsolete or untrustworthy. The Gallup survey from May 2016 shows a 78 percent disapproval rate of Congress, while an average of surveys presented by RealClearPolitics projects a 78.2 percent disapproval rate. Much of the reason for this disapproval is a sharp drop in the voters’ belief in the Members’ abilities to do their job. Constantly missed budget deadlines, stopgap extension measures and even shutdowns of the Federal Government have only served to deepen the citizen’s belief that Congress isn’t doing its job. This trend underlines the need for a reform of the budget process and the elimination of political gridlock.

As the August recess is already finished and the start of the next fiscal year on October 1 is approaching, a new wave of negotiations over the annual budget have taken on greater urgency. Being in the midst of the electoral season, the debate will become even more heated as the economic plans and campaign promises of the major presidential candidates will articulate the vision each party has for the future of the American economy, including the rate of economic growth, the size of government, levels of public spending, the size of the national debt and other variables that impact discretionary spending. (Under current law, most of the national budget is considered mandatory spending, such as Social Security and Medicare, and are not even considered in the annual budget resolutions.) Congress’ inability to pass a budget as established by the increasingly obsolete 1974 Budget Act is at the heart of the public’s dissatisfaction with our lawmakers.

There is an old maxim in Washington that says, “Elections have consequences.” As a political institution in the purest form, the Congress represents the will of the voting citizens through actions of negotiations and deliberations leading to legislative proposals and actions. The Constitution enshrines the core values of negotiation and compromise, yet these concepts have taken negative connotations in the modern Congress. The focus has shifted from negotiating and compromising to get the best deal possible, towards extreme polarization that seems more interested in scoring political points than actually coming up with a budget. Of course there is some degree of political gamesmanship in all budget negotiations, but up until fairly recently, Members understood when they had won as much as they could in negotiate, it was time to accept compromise and make the final deal. Lately, the compromises that make budget deals possible are not happening, leaving the Congress struggling with a host of gimmicks to keep the government running (usually) without actually agreeing to a budget plan, as required by law.

As a result of these political fights, Congress has squandered its political capital and became weak in the eyes of the public. There is also a paradoxical image where the disapproval rate is consistent with voters’ contempt for Congress’ deficiency but at the same time voters appear to support the idea of political brinksmanship in the name of ideological supremacy. According to a recent survey the Congressional Institute commissioned, one of the top concerns about Congress is the lack of accountability. The same survey found that the reason behind the lack of accountability is explained and interpreted differently. There are two positions that appear to be mutually exclusive: One states that Congress’ lack of accountability is related to a poorer legislative performance of Members, and the other group supports the idea that the Executive Branch has insufficient power and Members are just trying to block the actions of the President.

The discontent of voters manifested towards Congress is actually largely related to the outcome of budget negotiations and votes. Even though voters’ disapproval is generally a reflection of the poor performance of Members in general, in a strict sense, it is related to Members’ ability to steer their tax dollars towards guaranteeing a high performance in the departments, agencies and programs funded with their money. From this perspective the budget function of Congress is directly correlated to the accountability aspect of discretionary spending. Simply speaking, the public thinks the government wastes enormous amounts of money, and the congressional budget process increasingly makes Members look more like legislative Keystone Cops than the guardians of the people’s tax dollars.

Failures of the Budget Process

The process of authorizing and appropriating the government agencies and programs has become so burdensome that missed deadlines are the norm and government shutdowns are actually an annual threat. Putting aside the political reasons leading to the failure of the budget process, uncertainty regarding Federal budgets and government shutdowns are costly for everyone. As a result, there are few Members of Congress of either party who will defend the current budget process and not support some version of budget reform. Budget reform is not an easy task, since the budget, authorization and appropriation process affect every single aspect of governing, but there is no lack of proposals for changes that can be supported on a bipartisan basis in the House and the Senate. Since it is universally accepted that Congress cannot complete its budget work on time, a good starting point for reform would be changing the beginning of the government’s fiscal year from October 1 to January 1.

The genesis of the modern Presidential budget system is the Budget and Accounting Act of 1921 when the government incurred a $1 billion annual budget deficit (this is now known as “the good old days”). The provisions of the 1921 Act created the Executive budget process and the calendar for submitting the budget recommendations to Congress within a certain deadline. Although the foundations for the budgetary procedures were laid, our current budget process was a result of a dispute between the President and Congress over President Richard Nixon’s decision to impound (refuse to spend) funds he considered, wasteful rather than spend the money on environmental programs as lawmakers directed. In response, Congress passed the Congressional Budget and Impoundment Control Act of 1974, and Nixon, weakened by the Watergate scandal, signed it. At the core of the Budget Act of 1974 was the assumption that increased congressional responsibility of the budget process would result in a more orderly and efficient completion of the annual budget and greater congressional control over the nation’s purse strings. The Budget Act consisted of five aggregates: total outlays, total budget authority, total revenues, the deficit or surplus, and the public debt. Although the 1974 Act has been amended several times since its adoption, it remains the foundation of the current budget system.

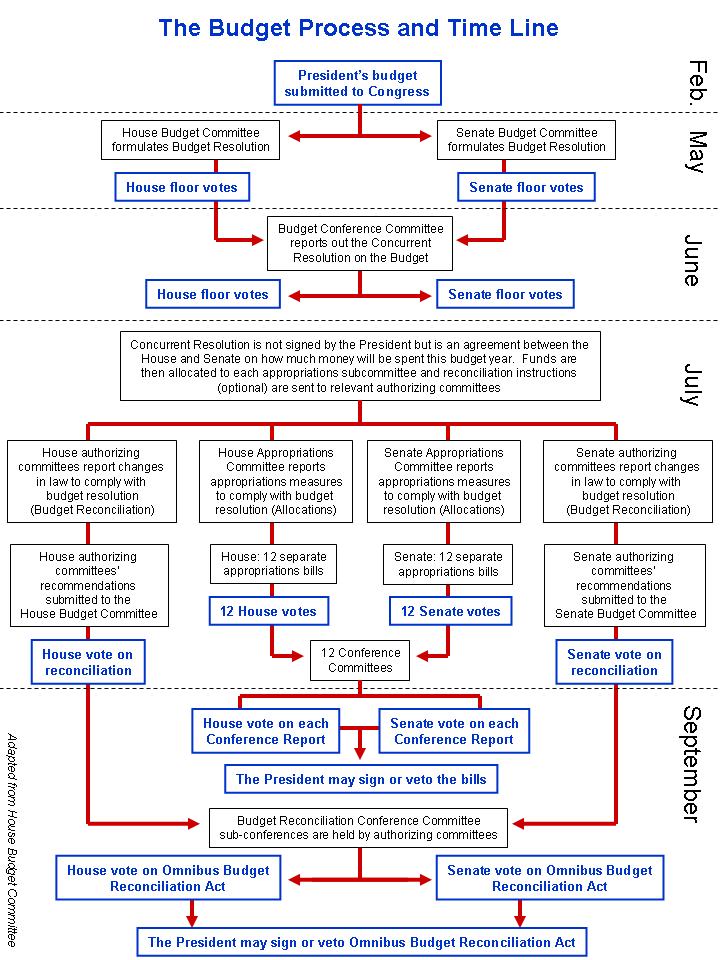

The 1974 Act coordinates “legislative activities on the budget resolution, appropriations bills, revenue measures, reconciliation legislation, and other legislation with budgetary effects”[1], and to achieve its purpose, it created specific calendar deadlines and procedures for the budget process. The budget calendar with the explicit time frames for submission, evaluations, and instructions for authorizing and appropriating is one of the most obvious problems in the current budget dysfunction. The Act sets the time frame for the budget procedures to be completed in Congress and for the President to sign the outcome into law. That is how the budget process is supposed to work. For several decades, these calendar deadlines have grown increasingly difficult for Congress and the Administration to meet, and indeed today, it is generally accepted that at the end of every fiscal year, Congress will have to pass some stop gap measure to buy more time to complete the annual budget process.

The budget procedures are set in a pyramidal way – the Constitution, Federal statutes and the rules Congress sets for itself. The legal provisions governing the current budgetary procedures are found in the enumerated powers listed in Article I, Section 8 of the Constitution, in the Federal Code with laws such as Budget Act of 1974 with its subsequent amendments, as well as the Anti-Deficiency Act, but also in the rules Congress enacts for itself (i.e., the rules that establish the committees and process for the consideration of spending, borrowing and raising revenues).

The Constitution clearly gave the power of the purse to the Congress, including the sole power to originate revenues, appropriate spending and borrow money, but it does not specifically direct how these legislative powers are to be exercised, much less establish a budget process. In fact, the United States government went nearly a century and a half before establishing any kind of formal comprehensive and annual budget process. The innovation of the 1974 Budget Act was to establish actual budget committees in Congress responsible for creating an annual budget blueprint and introduced requirements for a budget calendar, making these provisions legally binding. However, this Act does not mention any penalties in the event Congress did not pass a budget according to the Act (though in 2011 Republicans threatened to pass legislation that would suspend Member’s pay if they did not pass a budget).

One common denominator in both political parties’ frustration with the budget process is the time-consuming and complicated procedural steps that Congress must take in order to pass a budget resolution with a focus on the calendar set by the Budget Act of 1974. Although it was meant to create a clear time frame for each branch to complete its work, there just is not enough time, for both the authorization and the appropriation process to be completed. The President’s budget is sent to Congress in February and both Chambers must agree to the budget resolution by April 15. Authorization bills are really only given from April 15 to May 15 for consideration before the Appropriators are allowed to start passing their bills – all of which must be agreed to by both Chambers and signed by the President before the start of the fiscal year on October 1. As a result, the authorization process has increasingly been phased out, allowing the appropriation bills to be considered, in many cases, without the authorizations that are supposed to define what the appropriated money should be used for.

There are multiple examples of programs operating despite the lack of proper authorization. Just consider the case of the Department of Homeland Security, which was last authorized when it was originally created. But even the significant deviation from an authorization-appropriation model towards an appropriations-only model has not made it any easier for Congress to meet its schedule. The evidence of this is the common practice of continuing resolutions and omnibuses to carry over the previous annual spending bills until the House and Senate can agree and the President sign all appropriations bills. In fact, this has not occurred on schedule for 20 years. So one of the first things Congress needs to do is change the deadlines to a more reasonable time frame, and create a better coordination between the Executive and the Legislative Branches obligations for passing the budget.

Why Move the Start of the Fiscal Year to January 1?

January 1st would be a more realistic start to the fiscal year. Passing spending bills on time is the one action required by the Constitution. Failing to successfully meet the October 1 deadline has repercussions on both the Congress and the President, while the stop-gap measures required to compensate for missed deadlines has impacts on the public from the highly significant to the merely annoying. It is no way to run a government.

Congress is not alone in not meeting its deadlines. The entire process begins on the first Monday of February, when the President submits a budget proposal. Or in theory, it should start with that date. Practice and history have shown that budget submissions are often delayed, meaning Congress has even less time to pass its own budget and appropriation bills. President Obama was particularly bad with meeting his obligation to submit a budget proposal on time. In fact, in 2013 he was so late in submitting his proposal, that Congress was forced to guess what the President’s proposal would be and build its estimation on what could be nicely called an educated guess. But plenty of other Presidents have been late in submitting their budgets as well. This is another example in support of the idea that the calendar set in the Budget Act is not working.

Table 1: Too Much to Get Done in Eight Months – the Current Budget Cycle

Source: American GeoSciences Institute (http://www.americangeosciences.org/policy/overview-fiscal-year-2017-appropriations)

Changing the date of the fiscal year to the beginning of the calendar year is a first step towards addressing the issues of the calendar for the budget procedures as it is right now. The counterargument for that is that this is not a novelty in itself. The date had been previously changed, from July 1st to October 1st in the 1974 Act. Another argument against changing the date to January 1st is that it allows Congress to be less accountable by putting off tough decisions in election years until after the election (an argument easily dismissed by the fact that Congress has done exactly that for the last 10 election cycles).

Changing the date of the fiscal year to the calendar year would diminish the risk of government shutdowns, as the entire time frame for completing the works by Congress would be extended. Furthermore, it would be a measure of improving the time management in order to decompress the tight calendar existing under the current legal requirements. For Congress to complete all of the steps ensuring the 12 stand-alone spending bills to pass and guarantee that the authorization phase is not neglected, there needs to be a complementary measure to changing the date of the fiscal year in order to produce an overall improvement. Reverting back to the authorization and appropriation model is the key. Establishing a new model with time frames that would respond adequately to the changes in the government size, the economic projections and the expected priorities of funding is the embodiment of the budget reform idea. The arguments for extending the fiscal year based on actual experience over the last two decades is close to undeniable.

Conclusion

Changing the date of the fiscal year to January 1st is merely one component of a comprehensive budget reform. Congress is faced with severe mistrust from the electorate and the improper functioning of the budget process increases congressional disapproval. The idea of changing the fiscal year to the beginning of the calendar year comes from one fundamental principle: Restore the authorization-appropriation model. Stretching out the calendar will help Congress to pass the 12 annual spending bills and increase the amount of time for Congress’ authorizers to correctly evaluate the budget proposal submitted by the President and conduct the oversight necessary to make responsible authorization choices.

This measure would not solve the budget problem by itself, and should be considered in the context of a broader reform effort considered by a Joint Committee on Congressional Reform that considers changing to a biennial budget and enforcing the requirement to authorize Federal programs before they can be appropriated. The Joint Committee on Congressional Reform is needed for this effort, since the type of budget changes required affects so much of governing. It would be wrong, and probably impossible, for one party to dictate terms of reform to the other. To build a genuine consensus requires bipartisan and bicameral agreement, and for changes in law, a Presidential sign-off. Agreement on such an enormous task will not be easy, but there is nearly universal agreement that reform is needed. Changing the fiscal year would be a relatively simple way to start the reform process with bipartisan agreement and cooperation.

[1]Ryan P., “The Federal Budget Process, A Brief History Of Budgeting In The Nation’s Capital”, December 7, 2011, http://budget.house.gov/uploadedfiles/bprhistory.pdf